All Local, All The Time

All Local, All The Time

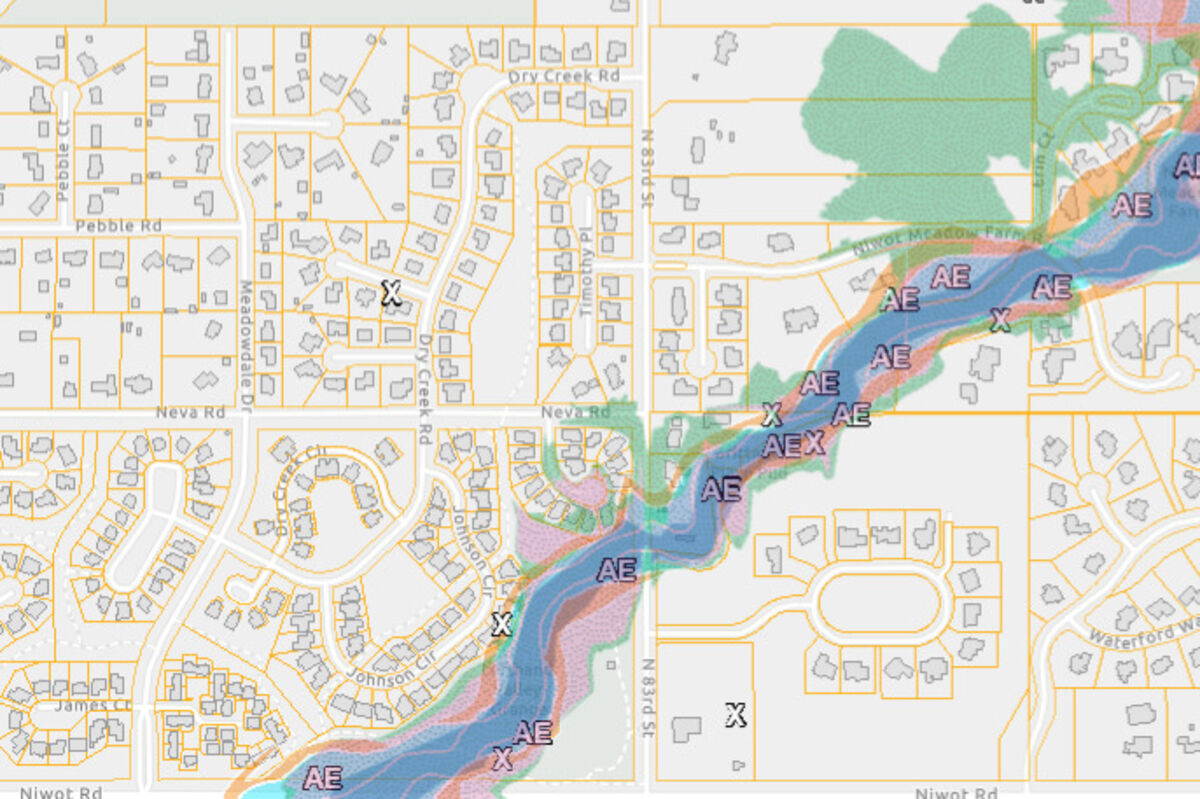

Official regulatory floodplain in Niwot

Readers of last week's Courier won't be surprised to learn that FEMA will soon be implementing new floodplain maps for Boulder County.

But what does that actually mean for the average homeowner?

Some Niwot residents along Dry Creek have lived in a floodplain for years. They attended the county's Jan. 16 information session with one question--would they be required to make changes to their property in response to the new maps?

The simple answer is "no." But Boulder County has received a federal grant to conduct the Floodplain Partners pilot program. This program will help homeowners evaluate if one of three options would reduce their flood damage risk--elevation, relocation or buy-out. Eligible property owners could then apply for federal funding to facilitate one of these solutions.

Residents reviewing the flood maps will notice two major demarcations--blue (1% annual chance of flooding) and yellow (0.2% chance of annual flooding). People often think of these likelihoods in terms of "100 year flood" and "500 year flood," but floodplain intern Casey Bangs encourages them not to. "This lets us think, oh, we just had a big flood, we won't have another one for 100 years... Mother Nature doesn't work that way."

Homeowners residing in the high risk flood zone (all A zones, or blue zones) are required to have flood insurance. And the new maps will change that situation for some people. At this time, there are 1510 Boulder County homes situated in the floodplain. Four hundred and twenty of those are new since the last time the maps were drawn, but 396 homes were also removed from the floodplain area.

Those not living in a high risk area can still purchase flood insurance, and can usually do so at a significantly reduced price. This might be a good idea. In the 2013 flood, 35% of those affected were in a low to moderate risk zone. Certain factors contributing to flooding, such as debris from forest fires and clogged ditches, cannot be factored into the flood models.

The good news is, insurance requirements won't kick in until the maps go live in 2021. This presents some opportunities for homeowners now designated as living in the floodplain. If the maps go live in March 2021, homeowners can still buy a year's worth of insurance in February at a reduced premium. FEMA is also offering "newly mapped rates," which start low and gradually increase, to help homeowners make the transition.

National Flood Insurance Program regional manager Erin May mentioned that private flood insurance agencies sometimes offer better packages than FEMA, but she warned people to pay careful attention to their definition of a flood, which can be narrow.

Homeowners insuring through FEMA can reduce their rates by acquiring an elevation certificate. If this certificate proves that the lowest elevation of a structure is one foot above the flood risk line, insurance rates drop dramatically.

Though the new flood map won't be official until 2021, Boulder County is already regulating to the new data. Parts of the old flood maps date back to the 1970s or earlier, so the new maps are much more accurate. Until the new maps go live, Boulder County will regulate to the most conservative version.

But there is still time to amend the maps. During the formal appeal period, property owners can submit scientific or technical data that changes map results or proves mistakes. When this time arrives, there will be a form on the appeals page of county and city websites. Property owners can also submit a Letter of Map Amendment, which compares the lowest adjacent grade that hits a particular structure with the elevation of the 100-year floodplain.

There may also be changes to the maps when ongoing flood recovery projects are completed.

For those with more questions, the Boulder County website has detailed information, including dates for the remaining public informational meetings: https://www.bouldercounty.org/transportation/floodplain-mapping/stay-informed/.

Reader Comments(0)